The problem isn't just that small businesses skip cyber insurance. It's that many who do buy it choose policies based on price alone, without understanding what actually gets paid out when something goes wrong.

This guide breaks down what small businesses actually pay, what those premiums cover (and what they don't), the factors that move prices up or down, and how to make a purchasing decision you won't regret after a breach.

Key Takeaways

- Annual cyber insurance premiums for small businesses typically range from $500 to $5,000+, with basic coverage starting under $400/year

- Premiums depend primarily on industry, annual revenue, data volume, and existing security controls

- Coverage includes breach response, ransomware, legal fees, and business interruption

- Exclusions for nation-state attacks, social engineering, and unpatched vulnerabilities can leave serious gaps

- 82% of denied claims share one factor: missing or incomplete multi-factor authentication (MFA)

- Cyber insurance covers losses after an incident; it does not replace proactive security controls

How Much Does Cyber Insurance Cost for Small Businesses?

Cyber insurance has no fixed price. A small business could pay under $400 per year for a bare-bones policy or well over $20,000 annually for high-limit, comprehensive coverage. According to Insureon, the median is around $129/month ($1,552/year), with 71% of small businesses paying $200/month or less.

Two common mistakes drive poor outcomes: underinsuring by choosing the cheapest option without reading exclusions, or overinsuring by paying for limits and endorsements the business will never need. Underinsuring surfaces at claims time; overinsuring drains budget that could fund actual security improvements.

Entry-Level Coverage: $500–$1,500/Year

Policies in this range offer:

- Basic data breach response and notification costs

- Coverage limits of $100,000–$250,000

- Minimal incident response support

Best for: Solo operators, freelancers, and businesses with limited sensitive data exposure.

What's typically missing: Business interruption, regulatory fines, and meaningful ransomware coverage. A ransomware attack that shuts down operations for 24 days — the average downtime for SMBs — won't be adequately covered at this tier.

Mid-Range Coverage: $1,500–$5,000/Year

This is the most relevant tier for growing small businesses handling customer data. Coverage typically includes:

- Limits of $1M or more

- Business interruption losses

- Ransomware response and recovery costs

- Legal fees and customer notification

- Regulatory defense (varies by policy)

Best for: Businesses with 10–50 employees that handle payment information, client data, or operate in regulated industries. For dental practices, law firms, and accounting firms in the Phoenix Metro area that InVision serves, this tier is typically the right starting point.

Advanced Coverage: $5,000–$20,000+/Year

Required for high-risk industries or businesses with significant revenue. Healthcare cyber insurance alone ranges from $1,500 to over $10,000/year depending on practice size and patient record volume. This tier typically includes:

- Social engineering and wire fraud endorsements

- HIPAA regulatory fine coverage

- Dedicated incident response teams with pre-approved vendor panels

- Higher sub-limits for ransomware

Key Factors That Affect Cyber Insurance Premiums

Insurers price policies based on how likely a claim is and how expensive it could be. Your premium reflects a detailed picture of your specific risk — not just a generic industry rate.

Industry and Compliance Requirements

Regulated industries pay more. Healthcare and financial services organizations face premiums approximately 50% higher than market averages, driven by mandatory breach notification requirements, per-record regulatory fines, and higher claims severity.

For businesses in dental, legal, accounting, and manufacturing — sectors InVision Technology Solutions serves across the Phoenix Metro area — premiums land toward the higher end of their revenue tier, driven by sensitive client data and compliance obligations like HIPAA and PCI-DSS.

Revenue, Business Size, and Data Volume

Insurers use annual revenue as a proxy for breach scale and potential downtime losses. Higher revenue means higher recommended coverage limits — and higher premiums. Data volume matters too: storing 50,000 customer records at $170 per compromised record (IBM 2025) creates a materially different risk profile than storing 500.

| Business Revenue | Recommended Coverage Limit |

|---|---|

| Under $500K | $500K–$1M |

| $500K–$2M | $1M |

| Up to $5M | $1M–$2M |

| Up to $10M | $2M–$5M |

| High-risk, 100K+ records | $5M+ |

Security Posture and Existing Controls

Security hygiene is now the deciding factor in both pricing and coverage approval — and most small businesses underestimate how closely insurers scrutinize it before issuing a policy.

The controls that move premiums down (or keep coverage from being denied):

- Multi-factor authentication (MFA) across all accounts

- Endpoint detection and response (EDR)

- Weekly patch management

- Regular, tested data backups

- 24/7 network monitoring

- Employee security awareness training

- Documented incident response plan

Missing controls don't just raise premiums: they can result in outright denial. Incomplete MFA deployment is consistently cited as the leading reason for denied claims across the industry. Some insurers now require continuous monitoring or a 24/7 SOC as a precondition for coverage.

Businesses working with a managed IT provider like InVision Technology Solutions — which includes 24/7 monitoring via InWatch, weekly patch management, and proactive threat detection — enter the underwriting process with documented security controls that can directly improve both eligibility and premium rates.

Coverage Limits and Deductibles

Higher limits raise premiums; higher deductibles lower them. The tradeoff matters: saving $500/year by accepting a $25,000 deductible can backfire badly in a real incident. Match your deductible to what you could genuinely absorb out of pocket — not what looks good on paper.

What Cyber Insurance Actually Covers — and What It Doesn't

Two policies at the same price point can cover completely different risks — and the gaps rarely surface until a claim gets denied. Knowing what's actually in your policy before an incident is the only way to avoid that discovery.

First-Party Coverage: Your Own Losses

First-party coverage pays for costs your business incurs directly after a cyber incident:

- Forensic investigation — determining how the breach happened

- Breach notification — required notices to affected customers

- Credit monitoring services — for impacted individuals

- Ransomware payments and negotiation costs — including third-party negotiators

- Business interruption losses — revenue lost while systems are down

- Data restoration expenses — recovering or rebuilding compromised systems

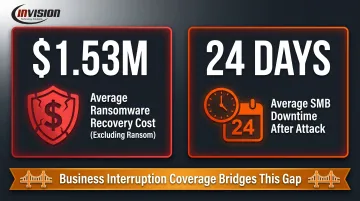

Business interruption coverage is particularly critical. The average ransomware recovery cost — excluding the ransom itself — sits at $1.53 million, per the Sophos State of Ransomware 2025 report. Average downtime for SMBs runs 24 days. A policy that doesn't cover income lost during that window leaves a gap most small businesses can't absorb.

Third-Party Coverage: Claims Against Your Business

Third-party coverage protects you when customers, partners, or regulators pursue your business after a breach:

- Legal defense costs and attorney fees

- Regulatory fines and penalties

- Settlements with affected clients

- Damages from failure to protect client data

For businesses in healthcare, legal, or accounting, this is often the most financially critical component. A single client whose confidential records are exposed can pursue claims well into six figures — and in regulated industries like healthcare or legal, regulatory penalties stack on top of those civil costs.

Common Exclusions Small Businesses Miss

The coverage above sounds comprehensive — until you read the exclusions. Standard policies routinely carve out scenarios that represent some of the most common real-world threats:

- Nation-state and war exclusions — Many policies exclude attacks attributed to foreign government actors. Following the Merck NotPetya settlement in January 2024, Lloyd's mandated new state-backed cyber exclusion clauses for all standalone cyber policies from July 2024 onward.

- Social engineering and wire fraud — Business email compromise and fraudulent wire transfers are frequently excluded or sub-limited in standard policies. This coverage requires a separate endorsement — important given that BEC and funds transfer fraud represented 58% of all cyber claims in 2025.

- Intentional acts and insider threats — Damage caused by a disgruntled employee is commonly excluded.

- Pre-existing vulnerabilities — If a breach exploits a known, unpatched flaw, some insurers may deny the claim.

- Ransomware sub-limits — Even a $5M policy may only reimburse $100K–$500K for ransom payments, regardless of the overall limit.

Budget vs. Premium Cyber Insurance: What Small Businesses Actually Get

A $500/year policy and a $4,000/year policy may look similar on the surface. The differences show up in the fine print — and in the claims process.

| Feature | Budget Policy (~$35–$100/month) | Mid-Range/Premium (~$145–$500+/month) |

|---|---|---|

| Coverage limit | $500K–$1M | $1M–$5M+ |

| Ransomware coverage | Sub-limited ($100K–$250K) | Higher sub-limits or broader coverage |

| Social engineering/BEC | Often excluded | Typically included with sub-limits |

| Incident response support | Basic or self-managed | 24/7 response, forensics, legal counsel |

| Regulatory defense | May be excluded | Typically included |

| Business interruption | Limited caps, longer waiting periods | Broader coverage, shorter waiting periods |

The gaps in budget policies correspond directly to the most expensive and common claim types. According to Coalition's Cyber Claims Report, ransomware losses averaged $269,000 per claim — well above the sub-limits most budget policies carry.

For most small businesses handling customer data, the mid-range tier delivers the best cost-to-coverage ratio. The right tier depends on your industry risk, data volume, and revenue — and the cheapest monthly premium often becomes the most expensive choice after a claim.

How to Get Better Coverage Without Overpaying

The right cyber insurance policy isn't necessarily the cheapest one — it's the one sized for your actual risk. Steps taken before you apply can directly lower what you pay.

Practical Steps to Reduce Premiums

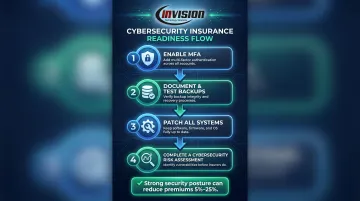

Take these actions before submitting an application:

- Enable MFA across all accounts — email, cloud services, financial systems, and remote access. This single control has the highest impact on both eligibility and pricing.

- Document and test backup procedures — insurers want evidence that backups exist and actually work, not just that they're scheduled.

- Patch systems fully — unpatched vulnerabilities are the leading cause of ransomware attacks and a basis for claim denial.

- Complete a cybersecurity risk assessment — identifying gaps before an underwriter does gives you time to remediate rather than explain.

Strong security postures can reduce premiums by 5% to 25%. Specific tools like Zero Trust platforms have been linked to rate decreases of around 10%.

Budget Estimation Framework

Rather than defaulting to the cheapest available option, calculate your coverage needs from three inputs:

- Records × $170 (IBM's average per-record breach cost) = minimum data exposure

- Average daily revenue × 24 days (average SMB ransomware downtime) = business interruption baseline

- Compliance obligations (HIPAA, PCI-DSS) = required third-party and regulatory coverage minimums

This gives you a realistic coverage floor to shop against.

Once you have that floor, the next step is knowing where your current security posture stands. InVision Technology Solutions offers a free Security Network Assessment for Phoenix Metro businesses — a practical way to identify gaps before an underwriter does. Their InWatch platform delivers 24/7 monitoring and weekly patch management that insurers increasingly treat as baseline requirements, so businesses can document active controls at application time rather than rush to implement them.

Frequently Asked Questions

What are common cybersecurity rules of thumb like the 1-10-60 rule?

The 1-10-60 rule, attributed to CrowdStrike, sets targets of detecting a breach in 1 minute, investigating in 10, and containing it in 60. It's a useful benchmark for incident response speed — especially given that organizations typically take 194 days on average just to identify a breach. Cyber insurance complements these goals but doesn't replace the security investment that makes them achievable.

How much does cyber insurance cost for a small business?

Most small businesses pay between $500 and $5,000 per year, with the median around $1,552 annually (Insureon). Very small operations can find basic coverage starting under $400/year. Premiums depend on industry, revenue, data volume, coverage limits, and existing security controls.

What does cyber insurance cover for small businesses?

Policies typically split into two categories: first-party costs (breach investigation, ransomware response, business interruption, data restoration) and third-party liability (legal defense, regulatory fines, client lawsuits). Specific coverage varies significantly by policy and tier — always read the actual policy language, not just the summary.

Does cyber insurance cover ransomware attacks?

Most mid-range and premium policies include ransomware coverage, but it's almost always sub-limited — typically $100K–$500K regardless of the overall policy limit. Some budget policies exclude or heavily restrict ransomware coverage. Confirm sub-limits and any named-actor exclusions before purchasing.

What steps can lower my cyber insurance premiums?

The top insurer-recognized controls are: enabling MFA on all accounts, maintaining tested data backups, patching systems regularly, and having a documented incident response plan. Businesses that demonstrate these controls during underwriting consistently receive better rates — potentially 5–25% lower than those without them.

Is cyber insurance worth it for a small business?

For businesses that handle customer data or depend on digital operations, yes. The average breach costs organizations under 500 employees roughly $3.31 million — against an average annual premium of around $1,500. At that ratio, it's one of the most straightforward risk transfers available to small businesses.