Introduction

Your company is growing. You're processing more financial data than ever, and someone from the finance team mentions "SOX compliance." For many IT professionals, the instinct is to forward that email to accounting and move on — but that's a mistake IT teams consistently pay for at audit time.

IT teams sit at the center of SOX compliance. Every financial system your organization runs, every access permission you manage, every backup you schedule — all of it feeds directly into what external auditors test.

According to GAO research, 689 restating public companies lost roughly $100 billion in market capitalization around initial restatement announcements alone. SOX was built specifically to prevent that kind of damage.

This guide covers what SOX compliance means for IT systems, which controls your team owns, and how to stay audit-ready year-round — so you're not scrambling when auditors arrive.

Key Takeaways

- SOX (Sarbanes-Oxley Act) is a U.S. federal law requiring publicly traded companies to maintain accurate financial reporting and strong internal controls

- IT teams own IT General Controls (ITGCs): access management, change management, computer operations, and audit logging

- CEOs and CFOs must personally certify internal controls quarterly; your IT documentation supports those certifications

- Non-compliance penalties reach $5 million in fines and 20 years imprisonment for willful violations

- Audits happen annually, but control testing and monitoring must run continuously year-round

What Is SOX Compliance?

SOX compliance means adhering to the requirements of the Sarbanes-Oxley Act of 2002 — a federal law enacted on July 30, 2002, with a stated purpose of protecting investors "by improving the accuracy and reliability of corporate disclosures made pursuant to the securities laws."

The Scandals That Sparked It

SOX emerged directly from failure — specifically, the high-profile accounting collapses of the early 2000s involving companies like Enron, WorldCom, and Tyco. Fraudulent accounting, weak oversight, and non-existent internal controls wiped out billions in investor wealth.

Arthur Andersen, one of the Big Five accounting firms at the time, ceased operations as a direct consequence of its role in the Enron scandal. Congress responded by passing SOX to make that kind of systemic failure legally indefensible going forward.

The Core Obligation for IT

To be SOX compliant, public companies must:

- Implement internal controls over all financial data and reporting systems

- File regular SEC reports with officer certifications attesting to the accuracy of disclosures and the effectiveness of controls

- Pass an independent annual audit by a registered public accounting firm

SOX is a financial regulation, but IT systems are the backbone of all three requirements. Reliable systems make accurate reporting possible, and access controls with audit logs give auditors the evidence they need to verify that those controls actually worked.

Who Must Comply With SOX?

SOX compliance reaches further than most people expect — it covers more than just large public companies.

Directly required to comply:

- All U.S. publicly traded companies (issuers under securities law)

- Their wholly-owned subsidiaries when those subsidiaries' systems affect consolidated financial reporting

- Foreign companies listed on U.S. exchanges or doing business in the U.S.

- The registered public accounting firms that audit them (overseen by the PCAOB)

Indirectly affected:

- Private companies preparing for an IPO — once a registration statement becomes effective, Exchange Act reporting requirements apply. Section 12(g) can also trigger registration for private companies that exceed $10 million in assets with a sufficient number of equity holders

- Private service providers whose systems touch a public company's financial reporting — PCAOB AS 2601 requires auditors to consider controls at service organizations when those services affect the user organization's internal control

That second point is where the indirect scope has real audit implications. If your IT team supports clients in finance, legal, or healthcare, their auditors may come to you — requesting evidence of your access controls, change management processes, or data handling practices.

Key SOX Sections Every IT Professional Should Know

Three sections of SOX drive the majority of IT compliance work — and each one creates direct, measurable obligations for IT teams.

Section 302 — Corporate Responsibility for Financial Reports

The CEO and CFO must personally certify the accuracy of every annual and quarterly report filed with the SEC. That certification includes an attestation that they have evaluated internal controls within 90 days before the report.

This creates a direct quarterly pressure on IT teams. Those certifications aren't possible without documented, functioning IT controls supporting the financial systems those reports draw from.

Section 404 — Management Assessment of Internal Controls

Section 404 is where most IT work lives. It requires organizations to document, implement, and test internal controls over financial reporting (ICFR) annually. Under Section 404(b), an external auditor must also attest to management's assessment — which means auditors independently test whether controls are both well-designed and actually operating.

PCAOB Auditing Standard AS 2201 governs how auditors test these controls. It explicitly identifies three IT general control (ITGC) categories auditors examine:

- Access to programs and data — who can view, modify, or interact with financial systems

- Program changes — how software updates and configuration changes are managed and approved

- Computer operations — job scheduling, data backups, and incident response procedures

Any control weakness identified here has consequences. A material weakness (defined as a deficiency where there's a reasonable possibility that a material misstatement in financial reporting could go undetected) must be disclosed publicly in SEC filings. That disclosure triggers regulatory scrutiny, reputational exposure, and potential market impact.

Section 802 — Record Retention and Document Tampering

Knowingly altering, destroying, or falsifying records to impede a federal investigation or SEC proceeding carries up to 20 years imprisonment. IT teams are responsible for ensuring that financial records, audit trails, and system logs are securely stored, indexed, and accessible. The seven-year retention rule under SEC Rule 2-06 applies to auditor records specifically — but your audit log retention policies need to align with this standard.

What Are SOX IT General Controls (ITGCs)?

ITGCs are the foundational policies and procedures governing the systems that support financial reporting. They're not a framework someone invented — they're what external auditors are looking for when they test your environment under Section 404.

Access Controls

The most heavily tested ITGC category. Auditors examine who can access financial systems, databases, and reports — and what they can do once they're in.

Key controls auditors expect to see:

- Least privilege enforcement across all financial systems

- Role-based access permissions with documented rationale

- Multi-factor authentication (MFA) on financial applications

- Periodic access reviews to remove stale or excess permissions promptly

- Documented processes for onboarding and offboarding users

Change Management

Change management controls govern how updates to financial systems are tested, approved, and deployed. An unauthorized or untested change to a financial application can introduce errors that go undetected, which is precisely the risk SOX is designed to prevent.

Auditors look for:

- Formal change request and approval processes with documented sign-offs

- Separation between development and production environments

- Evidence that changes were tested before deployment to production

- Rollback procedures for failed changes

Computer Operations and System Availability

Financial systems need to be available, reliable, and recoverable. This category covers the operational controls that keep them running.

Auditors will specifically test whether:

- Backups run on schedule and are verified

- Disaster recovery and business continuity procedures have been tested, not just written

- Incident response processes exist and are followed

- Job scheduling for financial processes runs as designed

Continuous operations monitoring is a practical way to satisfy this category. InVision Technology Solutions' InWatch system monitors servers, desktops, and network devices around the clock, with proactive alerting that surfaces issues before they affect financial system availability — a direct fit for Phoenix Metro accounting and financial services firms building their ITGC program.

Audit Logging and Monitoring

SOX requires comprehensive, tamper-resistant logs of system access and changes to financial data. These logs support auditor testing and must be available on request. Given the seven-year retention standard, log management is a long-term infrastructure commitment, not an afterthought.

Real-time monitoring tools that flag anomalous access patterns or unauthorized changes add a meaningful layer on top of log retention — giving your team the ability to detect and respond to issues before they appear in an auditor's findings.

SOX IT Compliance Checklist and Best Practices

SOX compliance fails when organizations treat it as an annual sprint. The companies that perform best in audits run compliance as a continuous operational discipline.

Internal Controls Setup

Start with the foundational baseline auditors expect to see:

- Document your control framework — align with COSO (recognized by the SEC for ICFR assessments) or COBIT for IT-specific governance

- Enforce least privilege and MFA across all financial systems and supporting infrastructure

- Establish formal change management with documented approval workflows and production/development environment separation

- Test and document backup and disaster recovery procedures — not just the schedule, but actual recovery test results

Ongoing Monitoring and Third-Party Risk

A solid baseline degrades fast without continuous oversight.

- Monitor IT systems and user access continuously — don't wait for the annual access review

- Maintain a vendor register for all third-party providers with access to financial systems; assess their security posture on a defined schedule

- Update control documentation promptly when systems, processes, or ownership changes — stale documentation is an audit finding

- Investigate anomalous access or change activity when flagged, and document that investigation

For smaller accounting and financial teams, the continuous monitoring burden is real. A managed IT provider can carry the 24/7 oversight — InVision Technology Solutions supports Phoenix Metro firms with SOX, PCI DSS, and GLB compliance through proactive monitoring and an average response time of 5 minutes.

Audit Preparation

Evidence gathering shouldn't start when the auditors arrive.

- Compile an in-scope system inventory before the audit window opens — every system that processes, stores, or transmits financial data

- Prepare evidence packages for each key control: system logs, screenshots, approval documentation, access review records

- Coordinate testing schedules with external auditors before fiscal year-end to avoid last-minute requests

- Resolve identified deficiencies before the formal audit begins — auditors will ask whether you found issues and what you did about them

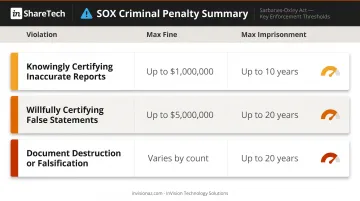

Penalties for SOX Non-Compliance

These aren't theoretical consequences. In 2019, the SEC charged four public companies with longstanding ICFR failures, with civil penalties ranging from $35,000 to $200,000 per company.

Criminal penalties under the statute are significantly more severe:

| Violation | Fine | Imprisonment |

|---|---|---|

| Knowingly certifying inaccurate reports | Up to $1 million | Up to 10 years |

| Willfully certifying false statements | Up to $5 million | Up to 20 years |

| Document destruction or falsification | Fine (amount varies) | Up to 20 years |

Material weakness disclosures also carry indirect costs: increased SEC scrutiny, potential investor response, and the operational burden of remediation under a spotlight.

Frequently Asked Questions

What is SOX compliance for IT systems?

SOX compliance for IT systems means implementing and maintaining the controls, access management, audit logging, and security measures that ensure the integrity of financial data. IT teams own the IT General Controls (ITGCs) that external auditors test annually under Section 404, which positions IT as a core compliance function rather than a supporting one.

What are the IT controls in SOX?

The four main ITGC categories are: access controls (who can access financial systems and what they can do), change management (how system changes are approved and tested), computer operations (backup, availability, and incident response), and audit logging and monitoring (tamper-resistant records of system activity).

Who needs to comply with SOX?

All U.S. publicly traded companies, their wholly-owned subsidiaries, foreign companies listed on U.S. exchanges, and the accounting firms that audit them must comply. Private companies preparing for an IPO also fall under SOX requirements once their SEC registration statement becomes effective.

What are the penalties for SOX non-compliance?

Executives who knowingly certify inaccurate reports face up to $1 million in fines and 10 years in prison; willful violations increase those penalties to $5 million and 20 years. Document destruction or falsification carries its own criminal charge of up to 20 years, and the SEC can pursue civil enforcement actions separately.

How often is SOX compliance audited?

SOX compliance is formally audited annually as part of the company's SEC filing, but Section 302 certifications occur quarterly. Internal control testing, access reviews, and continuous monitoring should run year-round — not just in the weeks before an audit.

What is a material weakness in SOX?

A material weakness is a deficiency in internal controls where there's a reasonable possibility that a material misstatement in financial reporting would go undetected. Material weaknesses must be disclosed publicly in SEC filings — so identifying and remediating control gaps before the annual audit is essential to avoiding a public disclosure event.